Google Adsense

Custom Search

Saturday, December 28, 2013

10 Leadership Tenets from Colin Powell

In a talk at Stanford GSB, former U.S. Secretary of State Colin Powell discussed his philosophy of leadership: http://stanfordbusiness.tumblr.com/post/71341426520/10-leadership-tenets-from-colin-powell

1. Successful leaders know how to define their mission, convey it to their subordinates and ensure they have the right tools and training needed to get the job done.

2. “Leadership is all about people…and getting the most out of people.”

3. Leaders should never show fear or anger. “You have to have a sense of optimism.”

4. Effective leaders are made, not born. They learn from trial and error, and from experience.

5. Leadership is about conveying a sense of purpose in a selfless manner and creating conditions of trust while displaying moral and physical courage.

6. A false leader is someone who fails to get the necessary resources for his or her staff to do their jobs.

7. “The best leaders are those who can communicate upward the fears and desires of their subordinates, and are willing to fight for what is needed. If not, the organization will weaken and crumble.”

8. When something fails, a true leader learns from the experience and puts it behind him. “You don’t get reruns in life. Don’t worry about what happened in the past.”

9. Good leaders must know how to reward those who succeed and know when to retrain, move, or fire ineffective staff.

10. “You know you’re a good leader when people follow you out of curiosity.”

http://daniel-j-stone.blogspot.com

(C) 2009-13

Friday, December 27, 2013

13 Things Mentally Tough People (Like Me) Avoid

From the Rush Limbaugh Show

BEGIN TRANSCRIPT

RUSH: Okay, now, mentally strong people, the 13 things they avoid. Now, here's how Forbes gets into them. "For all the time executives spend concerned about physical strength and health, when it comes down to it, mental strength can mean even more. Particularly for entrepreneurs, numerous articles talk about critical characteristics of mental strength -- tenacity, 'grit,' optimism, and an unfailing ability as Forbes contributor David Williams says, to 'fail up.'"

Do you know people that fail up? I do. My brother knows some. It really irritates him. Do you know people that fail up? The Democrat leadership's a classic example of people that fail up. That no matter what, everything ends up going well for them. No matter how bad they screw up, some people just have that knack.

"However, we can also define mental strength by identifying the things mentally strong individuals don’t do. Over the weekend, I was impressed by this list compiled by Amy Morin, a psychotherapist and licensed clinical social worker, that she shared in LifeHack," which is obviously a website. "It impressed me enough I’d also like to share her list here along with my thoughts on how each of these items is particularly applicable to entrepreneurs."

Now, I'm not gonna read all that. I'm just gonna touch on the 13 things. And, again, they are compiled by Amy Morin, psychotherapist, licensed clinical social worker. The 13 things mentally tough, strong people avoid. I don't know if they're in any order, but I'll share them with you in the order in which they are published.

Number one: They do not waste time feeling sorry for themselves. "You don’t see mentally strong people feeling sorry for their circumstances or dwelling on the way they’ve been mistreated. They have learned to take responsibility for their actions and outcomes, and they have an inherent understanding of the fact that frequently life is not fair," and they don't get bogged down in the unfairness of life.

Let me tell you something. If these things are not in order, that is a great one to be at number one. I can't tell you. That one dovetails with not giving people the power to offend you. I think mentally tough people realize that they're not like most people, and to get all worried about being offended or, "Gosh, this isn't fair," it's beneath people that don't have time for something like that. The reality of life is that most people are not considerate. Most people are doing nothing but thinking about themselves all the time. So that's really, I think, a key element of toughness.

Number two: Mentally tough people do not give away their power. And that is part and parcel of not being offended all the time. "Mentally strong people avoid giving others the power to make them feel inferior or bad." Put up some boundaries and don't let that stuff affect you, especially if it isn't true. You know, if I could wave a magic wand and change people, it would be don't worry about what people think of you, particularly people that don't know you. People that don't know you, it doesn't matter what they think. You and what you think of yourself is what matters, and if somebody thinks things about you that aren't true, forget it. Nothing you can do about it, and it's a total waste of time to try to change that.

Number three: Shy Away from Change. Mentally strong people embrace change and they welcome challenge. Their biggest “fear,” if they have one, is not of the unknown, but of becoming complacent and stagnant. An environment of change and even uncertainty can energize a mentally strong person and bring out their best.

Number four: Mentally strong people do not waste energy on things they cannot control. "Mentally strong people don’t complain (much) about bad traffic, lost luggage, or especially about other people." They don't experience road rage. You don't know what's going on in that car that may be driving erratically and running red lights.

Number five: Mentally tough people do not worry about pleasing others. There it is again. That's a variation of not worrying about what other people think of you. The thing is, you can't please other people. Well, it's everybody else's responsibility to be happy. Somebody's happiness is not your job. Somebody being content and happy is not your responsibility. And if you let somebody throw that off on you, you're gonna be miserable. If you're in a relationship, romantic relationship, marriage, anywhere at work or whatever, and if you let somebody make you responsible for their happiness, your goose is cooked.

A, you're dealing with somebody that can't be happy anyway. And number two, you can't do it. Happiness is an internal thing. Contentment is an internal thing, and it results from the pursuit of it. It doesn't just happen.

Number six: Mentally tough people do not fear taking calculated risks.

A mentally strong person is willing to take calculated risks. This is a different thing entirely than jumping headlong into foolish risks. But with mental strength, an individual can weigh the risks and benefits thoroughly, and will fully assess the potential downsides and even the worst-case scenarios before they take action.

Number seven: Mentally tough people do not dwell on the past. There is strength in acknowledging the past and especially in acknowledging the things learned from past experiences—but a mentally strong person is able to avoid miring their mental energy in past disappointments or in fantasies of the “glory days” gone by. They invest the majority of their energy in creating an optimal present and future.

Number eight: Mentally tough people do not make the same mistakes over and over again.

We all know the definition of insanity, right? It’s when we take the same actions again and again while hoping for a different and better outcome than we’ve gotten before. A mentally strong person accepts full responsibility for past behavior and is willing to learn from mistakes. Research shows that the ability to be self-reflective in an accurate and productive way is one of the greatest strengths of spectacularly successful executives and entrepreneurs.

Number nine: Mentally tough people do not resent other people's success. That's a toughie because human nature is such that -- I mean, somebody that fails up, you're gonna resent them. That's a tough one.

It takes strength of character to feel genuine joy and excitement for other people’s success. Mentally strong people have this ability. They don’t become jealous or resentful when others succeed (although they may take close notes on what the individual did well). They are willing to work hard for their own chances at success, without relying on shortcuts.

Number 10: Mentally tough people do not give up after failure.

Every failure is a chance to improve. Even the greatest entrepreneurs are willing to admit that their early efforts invariably brought many failures. Mentally strong people are willing to fail again and again, if necessary, as long as the learning experience from every “failure” can bring them closer to their ultimate goals.

Number 11: Mentally tough people do not fear time alone. "Mentally strong people enjoy and even treasure the time they spend alone. They use their downtime to reflect, to plan, and to be productive. Most importantly, they don’t depend on others to shore up their happiness and moods. They can be happy with others, and they can also be happy alone."

Number 12: Mentally tough people do not think the world owes them anything.

Particularly in the current economy, executives and employees at every level are gaining the realization that the world does not owe them a salary, a benefits package and a comfortable life, regardless of their preparation and schooling. Mentally strong people enter the world prepared to work and succeed on their merits, at every stage of the game.

And number 13: Mentally tough people do not expect immediate results.

Whether it’s a workout plan, a nutritional regimen, or starting a business, mentally strong people are “in it for the long haul”. They know better than to expect immediate results. They apply their energy and time in measured doses and they celebrate each milestone and increment of success on the way. They have “staying power.” And they understand that genuine changes take time. Do you have mental strength? Are there elements on this list you need more of? With thanks to Amy Morin, I would like to reinforce my own abilities further in each of these areas today. How about you?

I'm sure that Koko will find this story in Forbes. I've had it here since December the 10th. And it's written by Cheryl Snapp Conner, frequent speaker and author on reputation and thought leadership. She's got a newsletter you can subscribe to, but that's who the author of this piece is. So Koko will find it and put it up there. I heartily, as a really mentally tough guy, endorse this. (interruption) What is so funny? Are you disputing my assertion that I'm a mentally tough guy? Okay. Okay. I endorse all of these. There's no question.

END TRANSCRIPT

http://daniel-j-stone.blogspot.com

(C) 2009-13

Want To Succeed? Don't Check Your Email - And Work Out At Lunch

Erika Andersen, Contributor

David Morken practically sparkles with energy, even over the phone. Morken is Co-founder and CEO of Bandwidth, a 15-year-old company that focuses on IP-based communication technology – and is proud of the fact that they’re “challenging the standards of old telecom” in everything they do. Their stated mission is to unlock remarkable value for our customers – and, as I discovered when I spoke to him, Morken is convinced that a big part of doing that involves ‘unlocking remarkable value’ for their employees: making Bandwidth a place that supports employees’ body, mind and spirit.

One Bandwidth policy supports all three: the company has (and enforces) a total embargo on email to and from the company during vacation. That is, when you’re on vacation, you may not communicate with the company and they may not communicate with you. And to make sure the policy is followed to the T: when someone goes on vacation, all the folks he or she would ordinarily communicate with (employees, partners, boss, etc.) get an email, saying “so-and-so is on vacation. If he or she contacts you for any reason, please let us know.”

While it may sound a little draconian, it means that folks generally only break the rule once: getting a phone call from the CEO reconfirming that you’re on vacation and shouldn’t be emailing anybody seems to convince everyone that the policy is real. And, according to Morken, while lots of people have told him it’s difficult at first, no one has ever told him they think it’s a bad idea.

But what about the fast-charging, micromanaging execs who just say, “OK, then, I’ll stop taking vacation so I can stay on top of everything?” No dice: another Bandwidth policy is that you have to take all your vacation days, and you have to take them in the year you get them (no rolling over to never-never year).

The results? Employees experience vacations as vacations: rejuvenation, reconnection and relaxation. And managers put more attention toward developing their folks - because their folks can’t call them when there’s an emergency during their absence; they have to be willing and able to handle it themselves. Finally, Morken says, it makes managers more thoughtful about preparing for vacation: if you really can’t give added instructions or sort things out while you’re gone, it’s essential to get as much clarity as possible beforehand about what’s supposed to happen when you’re not there. He’s convinced that this has impact outside of vacation time, as well: that the increased clarity and trust ‘leak’ out into employees’ interactions every day.

Then there are the 90-minute lunches.

This part is voluntary vs mandatory, but it’s still an important aspect of the culture. Any employee can take a (paid) one-and-a-half-hour lunch to pursue fitness. Not only will Bandwidth pay you for the time, they’ll pay your gym membership, shuttle you to the gym, provide access to a personal trainer, and offer you a comprehensive “know and go” assessment of your physical condition that gives you a foundation of information for getting in better shape.

It’s a big investment for a relatively small (400 employee) company – so what’s the payoff? Morken believes that because everyone has limited time outside of work to be a significant other, a parent, a friend, or to pursue other non-work passions, making time for fitness during work hours makes it more likely that employees will both get and stay fit, and have time to focus on the non-work parts of their lives – improving both morale and productivity.

These unusual policies seem to be paying off in terms of business results: Bandwidth is set to make $150M this year – up about 20% from last year – and they anticipate $200M in profitable revenues next year.

I love hearing about companies and executive teams that are willing to do more than just talk about creating a culture focused on supporting people to be their best: who are willing to put dollars into it and create policies that support it.

And I’d love to hear what you think. Is this kind of thing a good idea, a bad idea, or…it depends? Please share your insights and experiences…

http://daniel-j-stone.blogspot.com

(C) 2009-13

Saturday, December 14, 2013

Forecasting Methods for International Enrollment Management- My time as Center Director for ELS at Ohio Dominican University.

Individual Economic Summary: Forecasting Methods for International Enrollment Management

Daniel J. Stone

MBA Student, Ohio Dominican University

In June 2010, I relocated from my home state of South Carolina to Columbus, Ohio to open an Intensive English Program (IEP) on the campus of Ohio Dominican University (ODU). Typically, institutions of higher education will facilitate an IEP in-house such as English as Second Language (ESL) programs located on the campuses of Capital, Otterbein, Columbus State and The Ohio State for example. In the case of ODU, management of an ESL Program is outsourced by my former employer, ELS Educational Services (ELS). A third-party vendor, ELS is based out of Princeton, New Jersey and touts itself as the largest recruiter of international students for universities and postgraduate programs in the US, Canada, and Australia (ELS Educational Services, Inc., 2012). At the local level, ELS Language Centers is a private entity that provides English language training on college campuses throughout the US.

Forecasting methods were employed to analyze data to carry out ELS's mission which was to make a profit. In general, ELS has the belief that the more industrious a Language Center (LC), and doing so with as little of possible manpower, the more profitable it will be. This trait comes from the ELS’s parent companies of Benesse Corporation and Berliz Language School based in Tokyo, Japan. With a Japanese belief system coupled by a corporate office in New Jersey and in the case of ELS/Columbus, a district office in Seattle, Washington, not only were there communication and logistical gaps but there were also culture gaps. This goes without saying the different cultures that the LCs are expected to manage while trying to navigate ODU's politics and being understaffed by design. The margin for success under these conditions are small since in order to deliver satisfactory results in circumstances that required a major undertaking and a high level of labor intensiveness is determined on all parties involved to buy in and being able to execute.

While the challenges were great from 2010 to 2012 at ELS/Columbus, the LC was accredited by the US Department of Education and became the first International English Language Testing System (IELTS) Testing Center in Central Ohio. However, a direct correlation that demonstrates that this ELS's mission needs to be broadened to more than just making a profit is the high turnover of quality staff leaving to work at the other ESL programs in Columbus coupled by the resistance received by "ODU Working Group". The "ODU Working Group" comprised of direct hires of ODU and in theory were to bridge any gaps in services between ELS and ODU.

Looking back, resources were scarce as I moved forward at Center Director at ELS/Columbus in the Summer of 2010. For example, the time allowed to prepare the forecast for upcoming enrollment periods was only six weeks. In truth, this was more like 5 weeks since about a week was spent in Chicago at the "AD-CD Training". Then, there was the Fourth of July Weekend when my wife flew up from South Carolina to help me hunt for an apartment. With Ohio Dominican University's campus essentially a ghost town, much of those first six weeks were spent advertising, interviewing, hiring, and training new staff alone. As a result, forecasting was conducted simultaneously the first year of operations until ELS/Columbus had enough data from a local standpoint to even consider employing qualitative forecasting. Therefore naive forecasting was employed that first year since the future trends of enrollment could not be explained at ELS/Columbus until more data (time) was gained. Nevertheless, qualitative and quantitative forecasting techniques were employed in order for ELS to operate as a proprietary on college campuses such as ODU. Having a solid understanding of ELS's mission which is to optimize profit, I was well aware that ELS valued what ODU had to offer because it fit perfectly within ELS's model. ELS would be operating by using the least expensive method while achieving desire results: profit maximization.

Quantitative Forecasting- Causal Forecasting

ELS squeezes out inefficiencies and streamlines resources by using the Full-Time Enrollment (FTE) technique. This technique is essential to ELS since it ensures that the organization remains profitable by managing a LC's hiring needs (See PowerPoint). By taking the item to be forecasted, enrollment, teacher's work schedules, classroom space, textbooks, and other inventory are allocated based on the number of students enrolled at the LC. In short, the more students enrolled at a LC, the more teaching and administrative hours are available. For example, a student enrolled in a full-time program (120 hours per session) gets a count of "1". A student enrolled in a part-time program which is enough hours to maintain student visa requirements (80 hours per session) gets a count of "0.67". Lastly, a student that is enrolled in a part-time program which does not need to maintain student visa requirements (60 hours per session) gets a count of "0.50". The formula used to determine the hours per day that are allowed is calculated by the formula =IF(Total Full Time Enrollment Count<41,( Total Full Time Enrollment Count multiplied by 7.76+155.2),( Total Full Time Enrollment Count multiplied by 7.76+164.9))/(Number of days of instruction per session which is 20). Without the FTE technique, a LC is unable to consistently operate within financial standards while verifying that the students enrolled are in the correct program for the accurate length of time. While managing the present FTE, the future FTE is managed by controlling levels such as forecasting future students' enrollments.

Next, FTE is tracked by hours allowed with holidays factored in versus the hours scheduled that session. Known as the Cumulative Standard Tracker, the hours unused which are rolled over to the following sessions are banked for when the schedule can't be kept within the financial standards. For example, a schedule can't be kept within financial standards due to too many students per a class's academic standards. The maximum number of students for core classes are 15 students and 20 students for elective classes. At the end of the year, any banked hours that are unused are taken away and the new year starts at zero banked hours (See PowerPoint).

The Future Student Forecasting Enrollment (FSFE) technique allows tracking and forecasting to be kept in order (See PowerPoint). Due to the seemingly endless possibilities of a student's status coupled by tight units of enrollment measurements (four 4-week sessions equate to one semester at ODU). For example, in any given session, the following events can take place: A student will depart and return to their home country, a student will transfer to another school, a student will return to their home country with the intention to come back to ELS/Columbus school within the next five months (or have to get a new immigration document thru their nearest US Embassy), a student will take the next session off and stay in the US to apply at other universities or take prep exams for entrance into another university, or a student will take the next session off due to a medical condition such as pregnancy. Then there are the students that are coming to ELS/Columbus school for classes and will have to the following events take place: new incoming for the first time, transferring from another school to ELS/Columbus school, returning to ELS/Columbus school after being out of the country temporarily, returning to ELS/Columbus school after taking the previous session off, returning to ELS/Columbus school after taking time off due to a medical condition such as pregnancy. With so many students coming and going every four weeks, and the importance that ELS/Columbus have enough staff to meet the needs and over staffing is not an option due to ELS's mission of making a profit.

Qualitative Forecasting- Contractual Shortfalls, Overgrowth, and Ramadan

I learned very quickly that the "one size fits all" approach from the corporate and district levels did not work more times than it did work. Heartburn experienced that first year was later corrected with both qualitative and quantitative forecasting. Some examples of the how qualitative forecasting was employed the second year was by ensuring that ELS/Columbus had enough classroom space. In May 2010, I came to Columbus for the very first time for the final interview and offer. In meeting some of the "ODU Working Group", members of the ELS senior management, aka "Jury and Executive opinion" explained to the ODU employees that in the first year they should expect approximately 45 ELS students comprising of 15 students staying in the dorms on campus, 15 students staying with host families, and 15 students from the outside. When classes commenced at the start of the Fall 2010 semester, ELS had four students. By the end of the semester, ELS's enrollment grew to about 25. It had appeared that ELS's senior management would be correct in their estimate of 45 students the first year. ELS operates 13 four-week sessions meaning that during the Winter Break, ELS classes were in session. Between the semesters, ELS took on 40 students, mainly transfer students. Despite the horrid conditions that first Winter Break, ELS's enrollment had blown past ELS senior management's expectations. At the end of the Spring 2011 semester, ELS was forced to have classes on the main campus in the allocated spaces as well as empty spaces usually used by ODU. Between the semesters in July 2011, ELS/Columbus's enrollment ballooned to 140 students, nearly 100 more than ELS senior management forecasted a year prior. Since ODU's enrollment was next to nonexistent on the main campus between the semesters, ELS was able to used empty classrooms. From the start of the Fall 2011 semester, ELS fleshed out its oversized enrollment by using the empty classrooms at the LEAD building on Airport Road. To bridge the logistical gap, ELS and ODU entered into a joint venture for the next 12 months which comprised of the use of an ODU vans and drivers. In order to sell the point that this joint venture was sustainable, I was able to use data from the past year. By employing causal forecasting, ELS was able to carry out its mission of profit maximization by utilizing unused classrooms since LEAD students don't have classes during the day. ODU supplied the resources and ELS supplied the schedule and split the operational costs 50-50.

During the first Winter Break, ELS students did not have adequate food service since ODU failed miserably by not carry out contractual obligations. ELS/Columbus protected enrollment by moving completely off the main campus the second Winter Break and did not charge ELS students for meals. The only thing that was on the main campus over the Winter Break were dorm students. Since ELS/Columbus had the ODU Shuttle, ELS/Columbus dispatched the shuttle on a regular basis to the Easton Town Center where students picked up meals and shopped at Wal-Mart. Sometime in 2013, the four classrooms and 20-unit computer lab that ELS used as its only classrooms from 2010-2011 were vacated due to the poor conditions. Upon my first visit in May 2010, the classroom had issues with flooding and puddles of water near the walls. In July 2010, my first week on the job, a pre-accreditation official came to check out our spaces and was appalled by the conditions found in the ladies room. While the move completely off campus is surprising since ELS invested thousands of dollars to make that LC fit their model of being on the campus, six months into my time there, I was dreading life working in that basement. While the students are all off the main campus, the admin staff still work in that area. Three years into ELS's stay at ODU and they were forced to the adult education building as ODU suggested from the beginning. A lesson to be learned that it is better to listen to the advice of your host (when they speak up) than it is to continue to force the round peg into the square hole.

Ramadan, the main holiday for Muslims and 80% of ELS/Columbus's FTE proved disastrous the Summer of 2011. Fortunately, due to the newness of the ELS/Columbus student body, they were not able to return home at their scholarship's expense. Because of this, ELS/Columbus had enough FTE so that ELS/Columbus teachers' schedules were not affected. New students at ELS took it upon themselves to not attend class which was in violation of the student visa and terminated their studies on the campus of ODU. They were told that they had to transfer to another school or return to their home country which didn't fit their agenda. In the Summer of 2012, qualitative forecasting had to be employed effectively to ensure that there were no misunderstandings coupled by the fact that FTE would be substantially lower than in previous sessions. Students effected by Ramadan were given options and signed an agreement and based on the outcome of the options selected determined how many senior teachers could take off the session that was effected by Ramadan and get paid due to the amount of vacation hours accumulated.

To conclude, the importance of both qualitative and quantitative forecasting techniques allowed me as Center Director to manage the scarce resources at my disposal as well as the heartburn of rolling out a new program. Despite the obstacles, I was able to carry out ELS's mission by hiring staff on a just-in-time basis, utilize unused classrooms, maintain a manageable amount of inventory such as text books, predict the number of beds needed for the dorms and homestay pools. These forecasting techniques weren't just one-way for ELS's benefit. These techniques were used to provide information to ODU's top management for the their forecasting of upcoming fiscal schedules due to the significance of the income that ELS was generating on the campus of ODU.

References

ELS Educational Services, Inc. (2012). About ELS. Retrieved from ELS Language Centers official website: http://www.els.edu/en/AboutELS

http://daniel-j-stone.blogspot.com

(C) 2009-13

Friday, December 13, 2013

7 Reasons Employees Don't Trust Their Leaders

Employees-don't-trust-leaders. As the world mourns the loss of Nelson Mandela and commemorates his greatness as a leader, we would do well to remember that one of the many hallmarks of his leadership was trust. The greatest leaders in the world gravitated toward Mr. Mandela because he was genuinely trustworthy and his purpose was to support peace, prosperity and unity not only in South Africa – but throughout the world. Mandela was able to lead people in ways that many find impossible to do. As he famously said, “It always seems impossible until it’s done.”

Unfortunately, trust is in rare supply these days. People are having trouble trusting each other, according to an AP-GfK poll conducted in November 2013, which found that Americans are suspicious of each other in their everyday encounters. Only one-third of Americans say most people can be trusted – down from half who felt that way in 1972, when the General Social Survey first asked the question. Forty years later, in 2013, a record high of nearly two-thirds says “you can’t be too careful” in dealing with people.

This same sentiment can be carried over into the workplace, where employees want their leaders to be more trustworthy and transparent. Employees have grown tired of unexpected outcomes resulting from the lack of preparation. They want to be informed of any change management efforts before – not after the fact. Employees desire to know what is expected of them and be given the opportunity to reinvent themselves, rather than be told they are not qualified for new roles and responsibilities and can no longer execute their functions successfully.

Leaders are challenged between informing their employees of the entire truth and holding back certain realities so as not to unnecessarily scare people or lose top-talent. More and more leaders today are being placed into uncomfortable moral dilemmas because they are attempting to salvage their own jobs while trying to maintain the trust and loyalty of their employees.

The growing tensions between leaders and their employees are creating productivity challenges as uncertainty becomes the new normal in the workplace. Furthermore, leaders are beginning to lose control of their own identities and effectiveness as their employees begin to lose trust in their intentions because of hidden agendas and political maneuvering – casting clouds of doubt over their futures.

Employees just want the truth. They have learned that the old ways of doing things just don’t apply (as much) anymore and more than ever they need their leaders to have their backs. Unfortunately, many leaders are operating in survival mode and don’t have the sphere of influence they once had; without leaders to sponsor and mentor them, high-potential employees must now figure out the changing terrain on their own.

Here are seven early warning signs to look out for so you can course-correct when employees are having trouble trusting their leaders:

1. Lack Courage

Leaders that don’t stand up for what they believe in are difficult to respect and trust. Too many leaders today battle the gulf between assimilation and authenticity. They waste too much of their valuable time trying to act like other leaders in the organization – rather than attempting to establish their own identity and leadership style. This is why less than 15% of leaders have defined and live their personal brand.

Perhaps leaders don’t believe that their employees are paying attention to this behavior – but they are intently observing. Employees are always in tune to what their leaders are doing and how they manage themselves. Employees know that if their leaders are not savvy enough to move themselves into a position of greater influence, it will make it that much more difficult for them to get noticed and discovered as well. The influence of a leader carries a lot of weight when it comes to how their colleagues judge and evaluate the potential of their employees.

When leaders lack the courage to enable their full potential and that of others, it becomes a challenge to trust their judgment, self-confidence, self-awareness and overall capabilities.

2. Hidden Agendas

Leaders that are too politically savvy can be viewed as devious and inauthentic. Employees want to follow leaders who are less about the politics and more about how to accomplish goals and objectives. While being politically savvy is important, leaders must be careful not to give their employees the impression of orchestrating hidden agendas.

Employees want to believe that their leaders are focused on the betterment of the team. If this requires well-intentioned political maneuvering to advance team goals and objectives, then great. However, if it comes across that a leader is solely intent on protecting themselves and their own personal agendas – trust from the team will be lost quickly and difficult to recapture.

3. Self-Centered

Hidden agendas make it difficult to trust that a leader’s intentions and decision-making are not self-centered. When a leader is only looking out for themselves and lacks any sense of commitment to the advancement of their employees – this shuts-off employees quickly. Great leaders are great coaches and are always looking to help their employees grow and prosper. When leaders lack any real desire to mentor, coach and/or guide the career advancement of their employees – it becomes increasingly difficult for employees to trust them. I’ve often said that leaders can’t go at it alone. But when leaders are too disruptive, their employees sense that they are in it for themselves and/or don’t trust the talent around them.

Also, when leaders are self-centered their ego stands in the way of advancing others – further eroding trust.

When people begin to speak negatively about their leader, it makes it more difficult for others to trust their intentions and vision. For example, look at what has happened to President Barack Obama since December 2009 when his approval rating was 69%. According to the Rasmussen Reports, four years later (as of December 7th), Obama’s approval rating is now at 43%. Nearly a 30% decline has created massive disruption to his reputation and many who have followed and supported him for years are now having troubling trusting him.

If you conducted a comparative approval rating survey in your workplace, how would your employees rate the performance of your leaders?

Every leader must be aware that they are constantly being evaluated and thus they can never grow complacent. When they do, this begins to negatively impact their reputation and the trust employees have in their leadership.

5. Inconsistent Behavior

People are more inclined to trust those who are consistent with their behavior. Isn’t it easy to begin questioning one’s motives/judgment when they are inconsistent? For example, I’ve worked with clients who appear to be on the same page – only to notice that they begin to disconnect when they believe that the direction of a project is not allowing them to mobilize their own agendas. In order words, when everyone but the leader is on board with a strategy – you begin to wonder if their intentions are to support the organization’s advancement or their own.

Leaders who are consistent with their approach and intentions are those who can be trusted. This is why so many leaders need to refresh their leadership style before they lose the trust of their employees.

6. Don’t Get Their Hands Dirty

Leaders must touch the business, just as much as they lead it. When leaders are over-delegating and not getting their hands dirty – employees begin to question whether or not their leader actually knows what is required to get the job done. Distrust amongst employees begins to rise.

Though leaders cannot be expected to have all of the answers – they should not play at arms-length either. The 21st century leader must be more high-touch in order to effectively evaluate the business and coach-up their employees. How else can a leader establish the standards to maintain and improve workplace performance?

Are your leaders getting their hands dirty or are they merely acting the part?

Leaders must earn the trust of their employees and stop believing that their titles, roles and responsibilities automatically warrant trust from others.

7. Lack a Generous Purpose

When a leader doesn’t genuinely have your best interests at heart, it’s difficult to trust them. When leaders are not grateful for your performance efforts – and are always attempting to squeeze every bit of effort they can out of you – it’s difficult to trust that they have intentions to be more efficient, resourceful and collaborative. Employees don’t ever want to feel taken advantage of – especially during a time when everyone is being asked to do more with less. Leaders must be more appreciative of their employees and more mindful of their endeavors.

Leaders who lack a generous purpose and are not compassionate towards their employees are difficult to trust. How can leaders expect their employees to give them everything they’ve got to increase their performance impact when they are not willing to do the same?

These seven behavioral traits are becoming much more prevalent in the workplace and if leaders fail to course-correct they will be putting their employees in positions of increased risk – disrupting their focus and the momentum of their careers.

This is what today leaders must consider: how to lead in new ways that focus less on oneself, but more on the betterment of a healthier whole. Leaders must enable positive social change through ethical innovation – what I call “innovation humanity.”

Let’s honor Mandela’s courage and compassion by letting his leadership inspire us now as it did throughout the life he lived with such generous purpose.

http://daniel-j-stone.blogspot.com

(C) 2009-13

Five Bosses You Don't Want (Or Want to Be)

December 09, 2013

By Jack and Suzy Welch

What is lousy leadership? Here are a few of the most common ways leaders can get it wrong and too often do.

The first and perhaps most frustrating way that some people blow leadership is by being know-it-alls. They can tell you how the world works, what corporate is thinking, how it will backfire if you try this or that, and why you can't change the product one iota. They even know what kind of car you should be driving. Sometimes these blowhards get their swagger from a few positive experiences. But usually they're just victims of their own bad personalities. And you and your company are victims, too. Because know-it-alls aren't just insufferable, they're dangerous. They don't listen, and that "deafness" makes it very hard for new ideas to get heard, debated, expanded, or improved. No single person, no matter how smart, can take a business to its apex. For that, you need every voice heard. And know-it-all leadership creates a deadly silence.

If know-it-alls are too in-your-face, a second kind of lousy leader is too remote. These emotionally distant bosses are more comfortable behind closed doors than mucking it out with the team. Sure, they attend meetings and other requisite functions, but they'd rather be staring at their computers. If possible, all the messy, sweaty people stuff would be delegated to HR managers on another floor. Like know-it-alls, this breed of leader is dangerous, but for a different reason. They don't engage, which means they can't inspire. That's a big problem. Leaders, after all, need followers to get anything done. And followers need passion for their fuel.

A third category of lousy leadership is comprised of bosses who are just plain jerks—nasty, bullying, insensitive, or all three. As one reader wrote us recently: "My boss is abusive, by which I mean disrespectful, finger-pointing, and sometimes even paranoid." Such leaders are usually protected from above because they deliver the numbers. But with their destructive personalities, they rarely win their people's trust. That's no way to run a business, which is why these types of leaders typically self-destruct. It's never as quickly as you'd hope, but unless they own the place, it does happen eventually.

The next type of lousy leadership is at the other end of the spectrum: It's too nice. These bosses have no edge, no capacity to make hard decisions. They say yes to the last person in their office, then spend hours trying to clean up the confusion they've created. Such bosses usually defend themselves by saying they're trying to build consensus. What they really are is scared. Their real agenda is self-preservation—good old CYA.

Which leads us to a final version of lousy leadership which is not unrelated: bosses who do not have the guts to differentiate. The facts are, not all investment opportunities are created equal. But some leaders can't face that reality, and so they sprinkle their resources like cheese on a pizza, a little bit everywhere. As a result, promising growth opportunities too often don't get the outsized infusions of cash and people they need. If they did, someone might get offended during the resource allocation process. Someone, as in the manager of a weak business or the sponsor of a dubious investment proposal.

But leaders who don't differentiate usually do the most damage when it comes to people. Unwilling to deliver candid, rigorous performance reviews, they give every employee the same kind of bland, mushy, "nice job" sign-off. And when rewards are doled out, they give star performers not much more than the laggards. Now, you can call this "egalitarian" approach kind or fair—and these lousy leaders usually do—but it's really just weakness. And when it comes to building a thriving enterprise where people have an opportunity to grow and succeed, weakness just doesn't cut it.

Surely we could go on, but we'll end here with a caveat. We hardly expect lousy leaders to read this column and see themselves. Part of being a lousy leader, no matter what the category, is lack of self-awareness. But if you see your boss here, take heart. When it's finally your turn to lead, you'll know what not to do.

Jack Welch is Executive Chairman at the Jack Welch Management Institute at Strayer University. Through its executive MBA and Welch Way management training programs, the Jack Welch Management Institute provides students and organizations with the proven methodologies, immediately actionable practices, and respected credentials needed to win in the most demanding global business environments.

Suzy Welch is a best-selling author, popular television commentator, and noted business journalist. Her New York Times bestselling book, 10-10-10: A Life Transforming Idea, presents a powerful decision-making strategy for success at work and in parenting, love and friendship. Together with her husband Jack Welch, Suzy is also co-author of the #1 international bestseller Winning, and its companion volume, Winning: The Answers. Since 2005, they have written business columns for several publications, including Business Week magazine, Thomson Reuters digital platforms, Fortune magazine, and the New York Times syndicate.

A version of this column originally appeared in BusinessWeek Magazine.

Photo: Jacom Stephens / Getty Images

http://daniel-j-stone.blogspot.com

(C) 2009-13

Thursday, November 28, 2013

Pricing Methods for a Municipal Government Event Center

Individual Economic Summary: Pricing Methods for a Municipal Government Event Center

Daniel J. Stone

Ohio Dominican University

In July 2007, I returned to my home state of South Carolina after being away for 15 years with the last three being in the Tokyo, Japan area as an English Teacher on the prestigious Japan Exchange and Teaching Program. With an undergraduate degree in Parks, Recreation, and Tourism Management, I eventually found work at the City of Greer in one of their newly created positions, Events Supervisor. On the mainstream level, the City of Greer was used as one of the props for the George Clooney movie, "Leatherheads" and since 1992, just outside of the City of Greer, German automaker, BMW has been manufacturing vehicles. Greer had just broke ground on a multi-million dollar construction project, Greer City Hall. This project included a multi-room events center, amphitheater, and gazebo (City of Greer, 2013).

My first assignment was to conduct market research to find out the fair market value for renting out the new spaces that were set to go online in the Fall of 2008. After meeting several times with the City Manager throughout the winter and spring of 2008, my findings were presented to the Greer City Council at the annual fee schedule meeting in the Summer of 2008. (Appendix A).

In retrospect, the City of Greer's new event center and park operated in a monopolistic competition environment. When local hotels and churches are included, there is a large number of event hall operators acting independently, market entry and exit was not difficult, services were differentiated by location, capacity of event hall and the ability to have an event hall expanded to two or three rooms and be able to use a kitchenette, for example. While customers chose among products, nonprice competition was essential as well. For example, a City of Greer resident received a discount.

Since a monopolistic competition environment has the characteristic of earning above normal profits which invites new entrants to the market, it appears that one other event hall began operations after the City of Greer's event center went online in October 2008. Furthermore, since new entrants will cause the City of Greer's demand curve to shift down and to the left and the Greater Greer supply curve to shift out and to the right, it is interesting to note that the prices that I presented in 2008 are the same in 2013 (Appendix B).

Considering that the position that I founded was eliminated among a few other newly created positions by the City of Greer due to the economic downturn known as The Great Recession of 2008, the supply and demand has not caused the prices to change. An existing competitor is still operating with business as usual. Barometric price leadership would suggest that one firm changes their price in response to economic conditions. But, five years and one of the most severe economic conditions since the Depression and the prices have stayed the same.

In conclusion, pricing of an event center managed by a government entity in a small town in the rural and small state of South Carolina comprises of the elements of a monopolistic competitor environment. Typically, the prices for goods and services will change depending on supply or demand. I suspect that due to the cumbersome nature of changing prices due to the annual fee schedule meeting coupled by the fact that the City of Greer benefits when other businesses such as their competitors are successful due to sales tax collections that the prices were set where they were desired by the Greater Greer area in 2008 and today. At the same time, if the City of Greer's event center does not remain profitable due to prices being too high, they can offset the loss with sales tax collections from the businesses in the municipality such as their competitors. Nevertheless, the City of Greer is serving its purpose as defined by Thomas Jefferson by enabling their residents a safe place to carry out an event. However, government entities are not businesses that are concerned with their bottom line and fall short in the implementation of money making activities. At present, the City of Greer's Recreation Department and Greenville Country Recreation District are at odds over the use of facilities and taxes to support those facilities (Greenville Online.com, 2013).

References

City of Greer. (2013). Events Center at Greer City Hall. Retrieved from City of Greer official website: http://www.cityofgreer.org/visit/events_center.php

Greenville Online.com. (2013). County-rec district merger expected to raises Greer taxes. Retrieved from website: http://www.greenvilleonline.com/article/20130620/YOURUPSTATE01/

306200056/County-rec-district-merger-expected-raises-Greer-taxes

Keat, Paul G. and Philip L.Y. Young, Managerial Economics: Economic Tools for Today’s Decision Makers, 6th Ed. New York: Prentice Hall, 2009.

http://daniel-j-stone.blogspot.com

(C) 2009-13

Friday, November 1, 2013

The 9 Essential Skills of Human Resources Management – How Many Do You Have?

HR Management

by Stephen Bruce, PhD, PHR

Tuesday, July 18th, 2006

By Jay Schleifer and Steve Bruce

When we interview a potential new hire, HR professionals assess the candidate against a list of key skills and personal characteristics needed for the job. Let’s turn the tables and see what that list of key attributes would look like for an HR professional.

In no way is our list authoritative, but it is the opinion of people, including BLR® Founder Bob Brady, who’ve spent decades meeting with HR professionals, supporting their goals, and reporting their achievements.

You may agree or not with our assessments, but either way, we’d like to hear about it via the “Share Your Comments” link at the end of the article.

That said, here goes:

HR Management Key Skill #1: Organization

HR management requires an orderly approach. Organized files, strong time management skills, and personal efficiency are key to HR effectiveness. You’re dealing with people’s lives and careers here, and when a manager requests help with a termination or a compensation recommendation or recognition program, it won’t do to say, “I’ll try to get to that if I have time.”

HR Management Key Skill #2—Multitasking

On a typical HR day, an HR professional will deal with an employee’s personal issue one minute, an intermittent leave question the next, and a recruiting strategy for a hard-to-fill job the minute after. And that’s to say nothing of social media, wage/hour, engagement, retention, and a whole host of other things, every one critical to someone.

In HR, if it’s not one thing, it’s another. Priorities and business needs move fast and change fast, and manager A who needs someone hired doesn’t much care if you’re already helping manager B who needs someone fired. You need to be able to handle it all, all at once.

HR Management Key Skill #3—Dealing with Grey

A surprisingly large percentage of the issues HR managers face are in “the grey area.” Is it discrimination? Is it harassment? What’s a “reasonable” accommodation? How far over backward do you have to lean to approve intermittent leave? HR managers have to be able to act with incomplete and “best available” information, and they have to know when to seek the professional help of colleagues, attorneys, and other experts.

See what everyone in HR is talking about every morning. Become a member of HR Daily Advisor and receive your FREE special report, 5 Mistakes Everyone Makes with Job Descriptions And How to Avoid Them.

HR Management Key Skill #4—Negotiation

Along with grey comes the need to negotiate—there are often two or more opposing views, and the successful HR pro can find an acceptable middle ground. Remember, the goal of negotiation is to end up with two parties that are satisfied with the outcome, and that’s not often easy to achieve.

HR Management Key Skill #5—Communication

HR professionals have to communicate up to management, over to managers, out to potential employees, and down to all levels of current employees. And they have to do it in writing, while speaking to large and small groups and, increasingly, through social media. They have to be convincing, caring, and believable.

HR Management Key Skill #6—Discrete and Ethical

HR professionals are the conscience of the company, as well as the keepers of confidential information. As you serve the needs of top management, you also monitor their actions toward employees to be sure that policies and regulations are followed. You need to be able to push back when they aren’t in order to keep the firm on the straight and narrow. Not an easy responsibility!

Of course, you always handle confidential information appropriately, and never divulge it to any unauthorized person.

HR Management Key Skill #7—Dual Focus

Employees expect human resources professionals to advocate for their concerns, yet you must also enforce top management’s policies. The HR professional who can pull off this delicate balancing act wins trust from all concerned.

There are times you must make decisions to protect the individual and other times when you protect the organization, its culture, and values. These decisions may be misunderstood by some, and you may catch flak because of it, but you know that explaining your choices might compromise confidential information. That’s something you would never do.

HR Management Key Skill #8—Conflict Management and Problem Solving

News flash! Everyone doesn’t always get along with everyone else. High productivity demands that people work together at least civilly. HR has to find ways to allow that to happen. And that’s to say nothing of the myriad other problems that hit HR’s in-box—you can’t be effective without problem-solving ability.

HR Management Key Skill #9—Change Management

Most companies today are in a constant state of flux. Task forces, matrices, and teams spring into being, do their jobs, and disband as others form. Hierarchies have been squashed, and companies have four or five generations working side by side. A lot of people are freaked out by what’s going on. HR has to help everyone cope with the constant changes.- See more at: http://hrdailyadvisor.blr.com/2006/07/18/the-9-essential-skills-of-human-resources-management-how-many-do-you-have-2/#sthash.sQRfRNUr.dpuf

http://daniel-j-stone.blogspot.com

(C) 2009-13

Sunday, October 13, 2013

Business education, Change management: The MBA is being transformed, for better and for worse

|

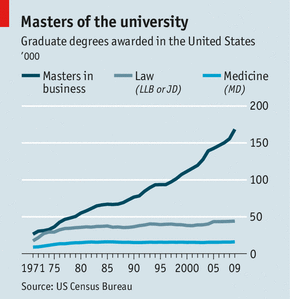

THE master of business administration is one of the success stories of our time. Since it was first offered by Harvard Business School (HBS) in 1908, the MBA’s rise has seemed unstoppable. Having conquered America, it reached Europe’s shores in 1957 when INSEAD, a French school, launched a programme. In the past couple of decades, Asia, South America and Africa have succumbed. Today, it is the second most popular postgraduate degree in America (after education).

Whereas 40 years ago, American colleges graduated similar numbers of lawyers and MBAs, nowadays nearly four times as many students pass out with a business-school master’s degree than with a law-school one (see chart). Although demand among Americans is plateauing, the slack has been taken up by emerging markets, particularly in Asia. India now has around 2,000 business schools, more than any other country. China has fewer, but their numbers are growing quickly. It has an estimated 250 MBA programmes, graduating around 30,000 students each year. This is less than half the number it will need over the next decade, according to Hao Hongrui of DHD, a consultancy.

Yet for all its success, these are demanding times. For a start, MBA candidates are beginning to question the return on investment of such expensive programmes. Business schools claim their graduates are less concerned than they once were about earning fabulous salaries. Instead of trumpeting the number of students who get high-paying jobs in finance, they now reel off examples of those who join non-profits or launch social enterprises. This fits the socially-aware image they wish to portray after the financial crisis.

However, there is a whiff of post-hoc rationalisation in this. Data from our latest ranking of full-time MBA courses (see article), show that the average basic salary of graduating students is now $94,000, around $1,500 less than it was five years ago. And yet our survey of business-school students suggests that they are more focused on the size of their pay-packets than those who enrolled before the crisis.

As salaries have fallen, tuition fees have risen. At Chicago, our top-ranked school, two years’ tuition costs $112,000, an increase of around $17,000 since 2008. Harvard’s prices have risen by nearly $25,000. A degree that once let the brightest students name their starting salaries now warrants a careful cost-benefit analysis.

Concentrate!

The MBA is changing in other ways, too. The days in which students study a broad set of management skills, with little specialisation, are numbered. Most business schools now encourage students to concentrate on one area, such as finance. An increasing number of MBA courses are tailored to particular industries, such as health care, luxury goods or, in one case, wine and spirits management.This is partly because students now have to have a clear career plan before they apply to business school. Competition for plum summer internships, the most common route to a post-MBA job, begins on the first day of school. Such is the focus on finding the right job, laments Sunil Kumar, dean of Chicago’s Booth School of Business, that students sometimes forget to savour the academic experience.

Business schools are expanding in other ways too. University administrators are wont to view them as cash cows and allow them to graze on other faculties accordingly. For years, they have been poaching professors from economics departments. Now they also woo psychologists and sociologists to teach softer subjects such as leadership and organisational behaviour. And their scope seems to be expanding.

“Big data” is currently one of the hottest study areas. York University in Canada, for example, recently launched a Master’s in Business Analytics. It recruits students with solid quantitative backgrounds, such as mathematicians and engineers, who spend half their time poring over mathematical models and half taking MBA classes. It is not enough to be a top-notch statistician nowadays, says Murat Kristal, director of the programme. Firms want people who can also understand the business implications of their analysis.

Perhaps the most disruptive influence on MBAs will be educational technology. Many institutions, from leviathans such as the University of Pennsylvania’s Wharton school to relative tiddlers such as Grenoble in France, now make some of their courses available free of charge as “massive online open courses”, or MOOCs. It is uncertain what long-term effect this will have. Roger Martin, the recently departed dean of Toronto’s Rotman school, clearly remains unconvinced: “Giving away your product? In what way is that a business?”

Instead, it is more likely disruption will be from better distance-learning technology. Demand for mass-market, paid-for but cheap online MBAs, delivered by institutions such as the University of Phoenix, is not new. However, it has been rarer for prestigious, traditional universities to offer distance-learning MBAs. This is changing. Top-ranked schools are spending heavily to equip themselves for this. Chicago, for example, has built video studios at its American campus so that students on its foreign campuses, in London and Singapore, do not miss its best tutors’ lectures.

The University of North Carolina at Chapel Hill (UNC) has gone further. It is one of the first top-ranked schools to offer a full-time MBA programme entirely at a distance. It has just enrolled 500 students in the second intake of its MBA@UNC programme, an online MBA that can be completed in 18 months. This is close to double the number it enrolls for its campus-based version. Interestingly, it typically costs a little more than attending Chapel Hill, partly because the technology has not come cheap. Yet students are signing up because they prefer not to give up their jobs, or because they cannot move to the campus for other reasons.

The tipping-point

Douglas Shackelford, the programme’s director, says that online classroom technology has now reached a tipping-point, whereby it is at least as good as a real classroom. Classes on the programme are limited to 15 students, spread across the globe, all of whom can interact. It has also allowed UNC to employ the best tutors whether or not they are in North Carolina. Professors lecture from India, France and across America. All lectures and class discussions are available in perpetuity, to be rewatched before exams or even after students graduate. Yet Mr Shackelford thinks he is only scratching the surface: “In 10 years we will look back and be embarrassed it was so simple.”This may come at a cost, however. As students get more choice, so business schools, perhaps for the first time, will be forced to compete on price, says Clayton Christensen, the Harvard professor who coined the idea of disruptive innovation. Many will find they do not have the resources, so there could, thinks Mr Christensen, be many casualties. Students might celebrate; business schools may prefer to keep the champagne on ice.

Saturday, October 12, 2013

The ITC eChoupal Initiative

The

ITC eChoupal Initiative

Daniel

Stone

Ohio

Dominican University

The ITC eChoupal

Initiative

Current situation

The

I.T.C. Limited, formally named India

Tobacco Company Limited, created the eChoupal due to an ineffective supply

chain for agricultural goods resulting in their International Business Division

lagging behind the other divisions of the company (Applegate, Austin, &

Soule, 2009). The harvest supplied by farmers were losing

60-70% of their value. This equated to

yields of 70% the value of global standards (Applegate et al., 2009). The reason for this were middlemen, formally known as commission agents

(CAs), who were reducing the profit margins for ITC (Applegate et al., 2009). Unfair practices with the farmers were

carried out by the CAs by using a crude weighing system that only accounted for

50% of the farmer's quantity (Applegate et al., 2009). Furthermore, farmers were not paid on time and in full as the law

required from the CAs.

Farmers would travel up

to a full day hauling their produce to the mandi (marketplace) to be auctioned (Applegate et al., 2009). Once at the mandi, the farmers had to wait an

additional two to three days before getting into the market (Applegate et al., 2009). At the mercy of the CA's low offers, the

farmers did not have a way to store unsold produce (Applegate et al., 2009). As a

result, the farmer would take his harvest to the winning bidder's shop to be

weighed (Applegate et al., 2009).

The farmers were

isolated and price discovery took place upon arrival at the mandi and was

received via mouth. If the farmer was

fortunate, while at the mandi, he would receive a large enough payment to cover

transportation costs, but had to settle for whatever he could get (Applegate et al., 2009). Weather reports were inaccessible, which

affected the farmer's harvest. Not

having to rely on the monsoons would allow the farmers to improve their crop

quality and streamline the process of

having it brought to the market (Applegate et al., 2009).

ITC Limited sought to remove the middlemen and provide an alternative to the mandi (Applegate et al., 2009). By doing this, the farmers were able to sell

directly to one of the ITC's 44 hubs (Applegate et al., 2009). The distance to the ITC hub was the same as the distance to the mandi (Applegate et al., 2009). However, at the ITC hub, ITC provided

compensation for transportation costs and had a retail outlet where farmers

could buy farming supplies and equipment.

Also, the ITC provided scientists and facilitated educational sessions

that demonstrated how the farmers could get more out of their crops by practicing

more effective methods (Applegate et al., 2009).

Also, the ITC sought to

rectify how the information was being delivered to the farmers (Applegate et al., 2009). This was achieved with the creation of

eChoupal, a website featuring weather reports, global crop standards, best

practices, market pricing from around the world, a Q & A forum, and the

news page (Applegate et al., 2009).

Current

Performance. ITC

Limited seeks to maintain its reputation as One of World’s Most

Reputable Companies by Forbes and a

Top 50 Asia’s Best Performing Companies by Business

Week. ITC

Limited employs over 26,000 people, at more than 60 locations across

India with approximately 6,500 eChoupals installed (Forbes Magazine, 2013).

Corporation

performance. ITC

Limited is considered one of India's most valuable corporations through

world-class performance, creating a growing value for the national economy and

ITC's stakeholders (Forbes Magazine, 2013).

For the ITC's agriculture business, is expected to invest

Rs 5,000 crore over 5-7 years in 2006 (ITC Limited, 2013). Because eChoupal has been able to preserve

product identity and manage product pricing, ITC has been able to gain market

share (ITC Limited, 2013). Chief

Executive Officer, S Sivakumar, states that the profitability of eChoupal will

be a challenge to measure due to an annual growth rate of 40% since 2005 (ITC

Limited, 2013).

Strategic Posture. ITC

Limited 's mission statement is "To enhance the wealth generating

capability of the enterprise in a globalizing environment, delivering superior

and sustainable stakeholder value" and has the vision statement to

"Sustain ITC's position as one of India's most valuable corporations

through world class performance, creating growing value for the Indian economy

and the Company's stakeholders" (ITC Limited, 2013). The objective for the eChoupal was to be an

improvement to the supply chain by serving as a delivery mechanism for its

agriculture business (ITC Limited, 2013).

As

a business strategy, ITC was committed beyond the market and did this creating

economic freedom in reengineering it's supply chain, fixing market

inefficiencies, information sharing, and product differentiation (ITC Limited,

2013).

In terms of an organizational strategy, ITC worked with

the village culture by having

transparent pricing, technology available at the village level, and a

waiting area at processing facilities. ITC

Limited provided reimbursement for transportation to the farmers and there was

no commitment from the farmers required to join ITC's eChoupal network (ITC Limited, 2013).

As an information strategy, it was imperative that there

was Internet access for remote villages.

ITC provided the villages an equipment kit comprising of computers,

connection lines, power supply, and a printer.

With these tools in the hands of the farmers, ITC provided technology

training to the farmers. To remove the

guesswork, ITC created pricing trends allowing flexibility for the farmers in

terms of when to sell their harvest.

Furthermore, to remove the fraud, waste, and abuse, ITC computerized the

weight process hereby eliminating the crude manual weight system, which had 50%

of the farmer's crop unaccounted for (ITC Limited, 2013). All of ITC's policies have the foundation of

trust, transparency, empowerment, accountability, control, and being an ethical

corporate citizen (ITC Limited, 2013).

External Environment Opportunities and

Threats

Societal

Environment. In evaluating the

external environment of opportunities and threats of the social relations

between ITC and those around, the economic, technological, political, legal, and sociocultural opportunities and

threats were examined. For example, one

of the technological opportunities was the introduction of new technology. Farmers were able to access the Internet,

which provided the economical opportunities of receiving market information (Upton

& Fuller, 2004).

Furthermore,

when the ITC streamlined the supply chain, this provided economical

opportunities of reducing costs for the farmers (Upton & Fuller,

2004).

While

the eChoupal Initiative provided many

economical and technological opportunities, the economical threat of negative

market change and the political and legal threat of government regulations

still loomed (Upton & Fuller, 2004).

Task Environment. The

threat of new entrants was low to moderate and the threat of substitute

products was moderate (ITC Limited, 2013). On the one hand,

the bargaining power of buyers was high. On the other hand, the bargaining

power of suppliers was moderate to high (ITC Limited, 2013). In terms of

rivals, the eChoupal Initiative competes against the mandi (Upton & Fuller, 2004). Other key factors

are opportunities for the eChoupal Initiative such as other products besides

the soybeans and wheat (ITC Limited, 2013). Also, environmental and weather threats still

present challenges to the task environment (Upton & Fuller,

2004).

Internal Environment

Strengths and Weaknesses

Corporate Structure. In

evaluating the internal environment of strengths and weaknesses, the corporate

structure at ITC was a system of management in which the decision making process was initiated at the highest level (ITC

Limited, 2013). ITC

Limited was organized on a basis of function, projects, and geography by

exercising its strengths of low transportation costs and not having a middleman

in the new format (Upton & Fuller, 2004). In addition to

this, the weaknesses of the ITC were exposed with IT equipment and hub

locations (ITC Limited, 2013). On the one hand, the ITC's structure was understood

and consistent with the strength of having the information exchange (Upton

& Fuller, 2004). On the other hand, the use of technology by the

farmers was a weakness of the structure (Upton & Fuller, 2004).

A similar comparison to ITC's

eChoupal Initiative, is the Apollo Tele-medicine Networking Foundation

(ATNF). Similar to ITC, ATNF has the

mission of "Bringing healthcare of international standards within the

reach of every individual" (The ATNF's vehicle to achieve this was the e-Health

program, which is similar to ITC's eChoupal (

Corporate Culture. The transparency of prices in the new format of eChoupal

was a strength for making ITC a well defined or emerging culture. Whereas, the education level of the farmers

was a weakness in this setting (ITC Limited, 2013).

ITC Limited's culture was consistent

with the objective of the eChoupal as

the vehicle to improve the

ineffective supply chain for agricultural goods with

the corporate strategy of the following:

"(a) create multiple drivers of growth by developing a portfolio of

world class businesses that best matches organization capability with

opportunities in domestic and export markets" and "(b) continue to

focus on the chosen portfolio including the agriculture business and Information Technology" (ITC Limited,

2013).

Corporate

Resources. ITC

Limited has research and development centers in two different locations in

India. In one location, the focus is on

product technology cells, common service modules, and advanced research

initiatives. At the other location, the

focus is on tobacco crop cultivation (ITC Limited, 2013).

Summary

of Internal Factors. ITC Limited believes that "One business derives strength

from another" (ITC Limited, 2013).

Also, ITC Limited created a diversified

conglomerate because this provided the opportunity to expand into an unrelated

set of businesses, whereby ITC has been able to link branding, trade marketing,

and distribution to create a competitive superior value proposition. Furthermore, the most important competency is

succession planning and ensuring that there is a clear plan at ITC (ITC

Limited, 2013). The

eChoupal has 70 warehousing hubs that are outsourced through service providers (Upton

& Fuller, 2004).

Analysis of Strategic Factors (SWOT)

Situational

Analysis. The most important internal factors from a situational

analysis was

ITC's support of the supply chain (Upton & Fuller, 2004). First, the use of

technology due to the delivery of computer kits to each village made it

possible for farmers to receive information that was transparent and in

real-time (Upton & Fuller, 2004).

Next, capitalization for the farmers was

essential in ensuring immediate cash payment at the fair market value to the

farmers and ITC made this possible (Upton & Fuller, 2004). The transactional

costs in the new format had low costs and the process was (Upton &

Fuller, 2004). Lastly,

the conversion of CAs to Samyojak made use of the key component of the supply

chain by educating and training the farmers with the use of the computers in

the villages and ITC hubs Upton & Fuller, 2004).

In terms of weaknesses, power

availability in the rural part of India was scarce. Consequently, the telecommunication

infrastructure was inferior (Bolton,

2013). Roads

were inadequate as vehicle access was limited.

Also, competitors attempted to divert produce from farmers (Upton

& Fuller, 2004).

The most important external factor from

a situational analysis was the new format that allowed for the supply chain

to perform more efficiently for the ITC's International Business Division (Upton

& Fuller, 2004). ITC Limited was able to sell products at the point of

sale when farmers brought in their harvest.

By doing this, ITC was able to access rural markets that were previously

in a difficult situation (Upton & Fuller, 2004).

In

terms of threats, the relationship between ITC and the Sanchalaks potentially

threatened ITC's supply chain. The

Sanchalaks acted as the hosts of the evening assemblies of information

gathering and distribution by the farmers.

The gatherings were uneven at times due to the demand of unwarranted

additional payments from the Sanchalaks.

These demands came due to the Sanchalak's homes being the site where the

computer kits were held (Annamalai, & Rao, 2003). Also, the new format took money and freedom

away from the middlemen, the Samyojaks. As

a result, the relationship between the Samyojak and ITC was strained in the new

setting (Annamalai, & Rao, 2003).

In terms of the present and future performance of the

eChoupal, the focus of the ITC is to grow for the future in a sustainable way (ITC

Limited, 2013). Therefore, the ITC needs

to focus on infrastructure development and innovation. These things will strongly affect the

corporation's present and future performance (ITC Limited, 2013).

First, infrastructure development will provide more hubs,

kiosks, and choupals, which will allow more convenience with the farmers (Upton

& Fuller, 2004). By doing this,

competitors will have more difficulty entering or competing in the market (Annamalai,

& Rao, 2003).

Next, the ITC needs to focus on innovation. By focusing on innovation, the ITC will

continue to provide beneficial information to its stakeholders, primarily the

farmers (ITC Limited, 2013). Also, ITC needs to be cognizant that they are

ahead of the continuous technological advances and are moving at a steady pace

that is consistent with the end users, the farmers at the eChoupal (Annamalai,

& Rao, 2003). While focusing on

innovation, ITC must also maintain the principles of transparency and trust (Upton

& Fuller, 2004).

Review Mission and

Objectives. ITC Limited should not

change mission or objectives since these address strategic factors and problems

by "enhancing the competitive power of the portfolio through synergies

derived by blending the diverse skills and capabilities residing in ITC's

various businesses" (ITC Limited, 2013).

Strategic Alternatives and Recommended Strategy

Strategic Alternatives

TOWS Matrix. In

regards to the TOWS Matrix, the strengths and opportunities, strengths

and threats, weaknesses and opportunities, and weakness

and threats are addressed.

From

a strengths and opportunities standpoint, one alternative strategy would be to use

strengths to maximize opportunities to introduce new technology for information

exchange. The

foundation for this is the computer kit

stationed at the Sanchalak's home in the farmers' village. To introduce

new technology, the utilization of mobile phones to